Saving money can be a struggle for many people.

This is because the cost of living keeps rising, the average income is stagnant, high-interest debt makes it difficult to save, and unexpected expenses keep coming up.

But let’s say you do make a good income… you may still struggle to save money due to lack of financial literacy, not creating or sticking to a budget, finding peer pressure hard to resist, or letting lifestyle creep increase your spending.

While these are real and valid reasons why it can be tough to save money… don’t let it hold you back from trying!

I used to come up with a million excuses to justify why I couldn’t save money. But I was too focused on blaming external factors for my financial situation instead of recognizing areas where I could improve.

In order to get good with money, I needed view challenges as opportunities instead of obstacles. I also needed to be willing to learn and understand that small steps over time is the key to mastery.

Another way I transformed my mindset was to repeat money mantras and affirmations to myself every day.

Below are three mantras that I tell myself (and perhaps you may find helpful too):

- Every day, I attract and save more money.

- I am grateful for the abundance that I have and the abundance on its way.

- Every action I take takes me closer to financial success.

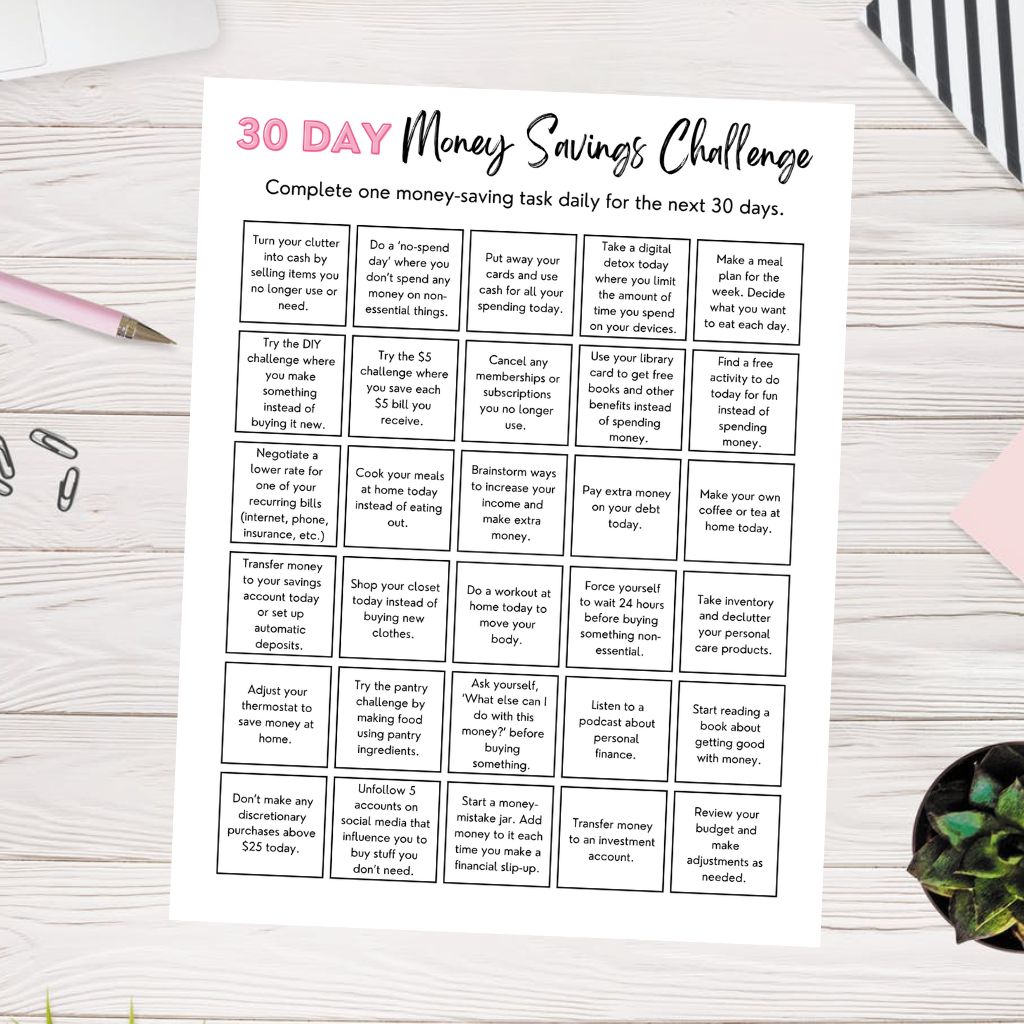

If you want to get good with money, I’ve created this fun savings challenge to help you save $1,000 in 30 days.

Each day, you’ll take an action step to help you save money and improve your financial situation.

This can help you reach your goals, such as building an emergency fund, paying off debt, or saving up for something fun.

If you want to track your progress, use you use this printable tracker to help stay motivated. It includes:

- A 30-day tracking worksheet where you can check off each money-saving task you complete.

- A 30-day blank tracking worksheet where you can create your own money-saving tasks.

- A savings tracker printable to help you save $1,000 in 30 days.

Table of Contents

Day 1 – Turn your clutter into cash

Is your closet bursting? Is your desk covered in piles of disorganized papers? Is your kitchen counter cluttered?

While sometimes a bit of mess can inspire creativity, many studies have shown that clutter in the home can lead to higher levels of stress which can make it hard to focus.

The average home has over 300,000 items. This is a treasure chest of potential opportunities to turn that clutter into cash.

With the right knowledge, you could easily find $1,000 worth of stuff to sell. This can be a great way to make extra money to help boost your savings or pay down debt.

The easiest way to find sellable clutter is to look for low-hanging fruit. This includes:

- Gifts that you’ve received that you don’t need or use

- Furniture that you don’t use anymore

- Gently used clothing that isn’t your style or doesn’t fit anymore

- Books and other collectables that are still in good condition

- Appliances that you no longer use or need

- Tools and gadgets that you don’t need

- Home décor or art in good condition

I made over $5,000 by selling my old stuff on Facebook Marketplace when I was moving to a new home.

The key is to take good-quality photos of the item you wish to sell, write a detailed description of the item so the right buyer can find it, and make the price attractive enough for someone.

It does takes time to list the items for sale, but it’s rewarding to free up space in your home and make extra money.

For the next 30 days, I encourage you to list and sell one item you no longer need each day.

You can put your earnings into a high-yield savings account. At the end of the month, you’ll have a tidier home and extra cash in your pocket.

Day 2 – Do a No-Spend day

A no-spend day means exactly that – you don’t spend any money on non-essential things.

This can free up money to use on other important things, such as building your emergency fund, paying down debt, or saving up for retirement.

While most people follow the no-spend challenge for a month (or longer), you can still benefit from doing a no-spend day.

I always do a no-spend month for January to help reset my finances for the year. By doing this challenge, it’s helped me to realize that the non-essential things I was spending money on wasn’t that important to me.

For example, I didn’t need to buy new clothes every month or go to Starbucks every day. This helped me cut back on these expenses going forward.

Below are some general guidelines on what’s allowed and what’s not allowed during a no-spend challenge. Of course, you can create your own rules and choose to just eliminate one or two spending categories.

By focusing on implementing a small change, this can help you stick to it in the long run.

Allowed:

- Only things that you absolutely need

- Rent, mortgage

- Utilities and other necessary housing expenses

- Transportation to get to and from work

- Essential groceries to put food on the table

Not Allowed:

- No coffee shops

- No restaurants or eating out

- No Amazon or online shopping (unless it’s for necessities)

- No clothes, shoes, or accessories

- No books, toys, or entertainment purchases

- No manicures or salon visits

- No plants

- Anything that you want, but don’t actually need

Read Next: How to do a successful low-buy year to save money

Day 3 – Use cash for all your spending today

Most of us use our debit or credit card to pay for our day-to-day expenses. But studies have shown that we tend to spend less when paying with cash.

This is because our emotions feel more pain when paying with cash.

As humans, we seek to avoid loses. When we physically have to count out notes and coins, it feels like we’re losing a tangible object.

On the other hand, nothing is handed over when paying with our card. By tapping or swiping, it feels less painful.

For example, let’s say you go on a day trip. You use your smartphone or smartwatch to pay for meals, shopping, and entertainment.

While this is a convenient way to pay, you don’t realize how much you’ve actually spent until you look at your bank statement at the end of the day.

However, when paying with cash you can physically see the money leaving your wallet and how much you have left to spend.

To help you save money, challenge yourself to use cash for all your spending today. Think about how much cash you’ll need to withdraw from the bank to cover your expenses for the day.

Each time you spend money, record the transaction. It can be done on a piece of paper, on a spreadsheet, or using a budgeting app.

Tracking your spending can help you see exactly where your money is going and help you make mindful decisions with your purchases.

Read Next: How to follow the cash stuffing budgeting method

Day 4 – Take a digital detox

Excessive media and technology can have a negative impact on our mental health and financial well-being.

Whether it’s the dozens of store emails that flood our inbox everyday or social media influencers that encourage us to buy things we don’t need, a digital detox can help restore balance and bring things back into perspective.

There’s no doubt that technology has given us tons of benefits, but it’s important to recognize when screen time is negatively impacting your relationships or overall wellbeing.

A digital detox is when you choose to reduce the amount of time you spend online or on your devices (TV, smartphones, computer, etc.) or disconnect completely.

I encourage you to try a digital detox for one day (or longer if you’re up for the challenge).

This can help you feel more content, become more productive, be more present and live in the moment, feel better about yourself, get healthier, sleep better, and rediscover offline activities.

Some goals you might want to consider include:

- Stop watching TV and using your phone by 8:00pm to improve your sleep.

- Leave your phone on silent when you’re with someone else so it doesn’t distract you from engaging in conversation.

- Leave your phone in another room when you’re working or studying to help improve your focus.

- Uninstall social media apps (Instagram, Facebook, TikTok, X, Pinterest) on your phone so you’re not mindlessly scrolling.

- Set a time limit to spend 1 hour max per day scrolling on social media.

A digital detox can help you save money because you won’t be tempted by influencers to make impulse purchases and you can use that spare time to focus on more productive things.

This may include things like planning your budget, decluttering your home, exercising, cooking a healthy meal, spending time with loved ones, reading a personal finance book, and so on.

Read Next: 45 things to do instead of spending money

Day 5 – Plan your meals for the week

An easy way to eat out less, save money on groceries, and reduce food waste is to meal plan.

This means you’ll sit down on Sunday (or whichever day works best for you) and plan your meals for the week.

Your meal plan can also include days that you plan to eat out, such as grabbing lunch with a friend or going out for dinner on the weekend.

You can also make a plan for all three meals (breakfast, lunch, and dinner) or just focus on planning out your dinners for the week.

I find it helpful to go through the weekly grocery store flyers to see what’s on sale. This can help you decide which items you need to buy and which items you need to use up at home (check your fridge and pantry).

If you need ideas, you can also use a service like Hello Fresh or the $5 Meal Plan.

Read Next: How to meal prep for a week – Beginner’s guide

Day 6 – Try the DIY Challenge

The DIY challenge is where you challenge yourself to make something instead of buying it new. This can help you save money and, in some cases, choose non-toxic options for your home.

Below are some DIY ideas you can try:

- Make your own all-purpose cleaner

- Make your own laundry detergent

- Make your own dishwasher detergent

- Make your own deodorant

- Make your own body scrub

- Make your own beauty products

- Make your own soup broth

- Make your own bread

- Recreate restaurant meals at home

- Sewing and mending clothes

- Making your own yogurt

- Cutting your own hair at home

I’ve been cutting my own hair for over 10 years now. I also make my own household cleaning products and deodorant.

Read Next: 20 zero waste swaps that’ll save you money

Day 7 – Do the $5 savings challenge

The $5 savings challenge is one of the easiest ways to save money. Each time you receive a $5 bill, you’ll save it. This can go into a savings jar, envelope, or you can transfer it to your savings account.

This savings challenge works best for those who use cash for their daily spending. It’s a low-effort way to boost your savings. Just by setting aside $5 a day will give you $150 in one month.

Day 8 – Cancel memberships & subscriptions you don’t use

Money leaks are small expenses that add up over time, sometimes up to thousands of dollars a year. One of the biggest leaks is paying for services and memberships that you don’t use anymore.

This includes gym memberships (Peloton), movie streaming services (Netflix), credit cards with an annual fee, paid apps, Amazon Prime, music streaming services (Spotify), shopping memberships (Costco), and so on.

Go through your bank statements for the past month and pay attention to your recurring bills. Some services are billed monthly, and some are billed annually.

If you use a service regularly, then go ahead and keep it. Just make sure to include it in your budget.

But for things that you don’t use, cancel it and put that money towards paying off debt or building your emergency fund.

You don’t need all the services at once. Instead, just catch up on one service at a time, such as Netflix, then cancel and try a different service next month.

It only takes a couple minutes of work to potentially save a lot of money each year.

Day 9 – Use your library card to get free books instead of buying

The library can save you a ton of money each year on books and magazines.

I used to buy books all the time and have been collecting them since I was a child. But after transitioning to a minimalist lifestyle, I decided to stop collecting items and sold over 300 books online.

Now, instead of buying new books, I always borrow them for free from the library. The only books I buy are cookbooks if I use it regularly.

Below are some more ways using the library can benefit you:

Free access to digital content – You can download eBooks, Audiobooks, and Magazines.

Free classes – You can learn something new by taking a free online course offered by the library.

Free entry to attractions and exhibits – Library card holders can visit select museums, attractions, and local exhibits for free.

Free in-library services – You can use your library card for in-house services such as the computer, print and copy machines, and some online resources.

Day 10 – Find a free activity to do for entertainment

Challenge yourself to find something fun and entertaining to do that’s also free. Below are some ideas to get inspired:

- Check out a local festival in your town or a nearby town

- Listen to a local band play live music for free

- Walk around an arts & craft fair

- Watch a local parade

- Visit a local park

- Get free passes from the library for local attractions

- Take a free class or join a free group at your local library

- Go hiking

- Learn a new hobby (watch YouTube video tutorials)

- Start your own garden

- Visit a free art exhibit

- Bake dessert or cook your favorite meal

- Have a movie marathon at home

Day 11 – Negotiate a lower rate for one of your recurring bills

Review your bank statement for the past few months and highlight all your recurring bills. These are goods or services that are automatically charged on a regular schedule – either monthly, quarterly, or annually.

You may be paying more than you should for your bills. For some expenses, it’s possible to negotiate a deal to pay less and save money.

Below are some bills that you can typically negotiate to reduce your household expenses.

Internet – Most plans offer a low introductory rate in the beginning. But after the first year, the standard rate will kick in, which is usually quite high.

Before your introductory rate is about to expire, this is the best time to negotiate a new deal.

Cable – Most people have switched to using streaming services like Netflix or Disney+. Due to this, you may be able to get a lower rate, especially if you say that you plan to cancel your service or switch providers.

Cell Phone – Many phone providers offer special promotions on holidays like Black Friday or Boxing Day. It doesn’t hurt to call and see which options are available to you, especially if you’ve been a loyal customer.

Review which services you use and how often you use them. For example, I don’t have a data plan because I work from home and there’s usually free Wi-Fi available at local stores and establishments.

Compare phone plans from alternative carriers that offer a lower monthly rate and see if your current provider can match their offer. Sometimes bundled options or family plans can also save you money.

Credit card interest and fees – If you carry a balance on your credit card, reducing your credit card interest fees can make a huge dent in your debt.

Car insurance – It’s important to review your car insurance policy once a year to make sure that it meets your needs for the best price.

Compare other insurance provider policies to see if they can offer you a cheaper rate.

Gym membership – Gyms usually offer promotions throughout the year, especially in January when many people are looking to join the gym. You can see if your current gym can match or beat the offer of another gym.

You may be able to negotiate a lower price if you pay upfront in full for the year, instead of paying month-to-month.

Day 12 – Cook your meals at home today

Restaurant prices have been outpacing grocery inflation over the past few years.

Despite the higher cost of groceries today, you can still save a lot of money by choosing to cook meals at home several times per week.

Challenge yourself to make all your meals at home today. Eating at home is also healthier because you can control the ingredients that go in your food.

Below are some tips to help you eat at home:

- Choose to cook quick and simple meals.

- Prep your food in advance (Overnight oats for breakfast, mason jar salads or soups).

- Take advantage of your slow cooker (Great for prepping meals in the morning so you’ll enjoy a hot dinner when you come home from work).

- Have dinner leftovers for lunch the next day.

- Choose frozen fruits and vegetables to save time and money.

- Freeze leftovers to enjoy another day (Great for things like soups, chilis, stews, and pasta sauce).

- Make ‘sheet pan’ recipes which are easy to prep and clean.

- Watch YouTube videos to learn how to make easy recipes

Read Next: 16 ways to slash your grocery bill in half

Day 13 – Brainstorm ways to make extra money

How would you earn money if you only had $5 and two hours?

This was a question that was given to a group of students at Standford University.

14 teams of students were given an envelope with $5. They could spend as much time as they wanted planning.

But once they opened the envelope, they only had two hours to make as much money as possible.

After the challenge was completed, each team was asked to give a 3-minute presentation to the class about what they achieved.

The typical answers were to gamble at a Las Vegas casino, buy a lottery ticket, or get supplies to set up a car wash or lemonade stand.

Gambling and buying a lottery ticket are a huge risk that comes with a small chance at earning a large sum of money.

Setting up a car wash or lemonade stand is a safe option for those who want to earn a few extra dollars.

But the students who made the most money didn’t use the $5 at all. They realized that focusing on the $5 narrowed their thinking and hindered their creativity.

Instead, they ignored the $5 and reframed the problem by asking themselves, how can we make money if we start with absolutely nothing?

To do this, one team recognized a common problem in small towns – long lines at popular restaurants on Saturday night.

Their solution was the make reservations at popular local restaurants and sell the reservations times (up to $20) to those who wanted to skip the lines.

Another team set up a stand in front of the school where they offered to measure bicycle tire pressure for free.

If the tires needed to be filled, they added air for $1 or requested donations instead of asking for a specific payment.

The team that made the most money though approached the problem from a different perspective. They realized that their biggest advantage wasn’t the $5 or two hours to earn money.

Instead, their most valuable asset was the 3-minute time slot to do their presentation in front of the class.

They created a 3-minute commercial for a company that was interested in recruiting Standford students and sold it for $650.

This story illustrates how to use tactics and strategy to achieve success. Each team was given the same resources: $5 funding and two hours.

The teams who made the least amount of money were too focused on the $5 and two hours, which distracted them from seeing the real value of the presentation time.

Think about this story in the context of your own financial journey. What are the $5 and two hours that are preventing you from using the best tactics and strategy to achieve your goals?

Read Next: 21 passive income ideas for beginners

Day 14 – Pay extra on your debt

Having debt can feel overwhelming and stressful. One way to manage that stress is to create a game plan to pay down debt.

If one of your goals is to live debt free, today’s challenge is to put extra money towards your debt payments.

If you don’t currently have debt, then you can put that money towards your savings instead.

Some of the best ways to pay off debt faster include:

- Paying more than the minimum.

- Paying off your most expensive debt first.

- Consider using the debt snowball method or the debt avalanche method.

- Paying more than once a month.

If you want to save the most money, consider following the debt avalanche method. This method helps you lower the amount of overall interest you may be paying.

You’ll continue to make the minimum payments on all your debts, then funnel any extra money towards the debt with the highest interest rate.

Once the high-interest debt is paid off, then you’ll focus on paying down the debt with the next highest interest rate.

If you’re motivated by seeing progress quickly, consider following the debt snowball method. This method helps build momentum as you tackle smaller amounts of debt first.

You’ll continue to make the minimum payments on all your debts, then funnel any extra money towards the debt with the smallest balance.

Once the smallest balance has been paid, then you’ll focus on paying down the debt with the next smallest balance.

Day 15 – Make coffee & tea at home

Making your coffee or tea at home may sound like trivial advice. This may only save you $2-5 a day or $1,000 a year – depending on how much your favorite cup of coffee costs.

$1,000 is still a decent amount of money in my books.

The key here is to focus on the mindset shift that’s necessary to reach your savings goals.

By making your own coffee or tea at home today, this can help interrupt auto-pilot spending habits.

For example, I used to grab a coffee on my way to work every morning because it was convenient. This become part of my morning routine and was an automatic spending habit.

Once I switched to making my own coffee at home, it took some time to get the taste just right. But now, I prefer the taste of my own coffee.

By making coffee most of the time at home, it feels like I’m “treating myself” and it becomes more special when I occasionally buy a coffee out.

Plus, it helps you to become more intentional about the little things. If you can be mindful about the small expenses, this can help you be intentional about bigger financial matters.

Now if your daily cup of coffee is the THING that makes you happy, then make sure to include it in your budget. It’s all about balance.

Read Next: 20 things I stopped buying to save money

Day 16 – Transfer money to your savings account

I don’t know about you, but when I see money sitting in my checking account, I’m more likely to spend it on silly things.

For me, the best way to prevent impulse purchases is to keep a “buffer” in my checking account and transfer the rest of the money to my high-yield savings account or investments.

For example, if you have a new bottle of shampoo, you’ll probably won’t think twice about how much shampoo you use.

But if there’s only a small amount of shampoo left in the bottle – and you don’t have time to buy a new one today – you’ll make sure to use those last few drops wisely.

Challenge yourself to transfer money to your savings account today. Even if you can only afford to transfer $10, that’s $10 more that you’re adding to your savings.

I keep just enough money in my checking account to cover my day-to-day expenses and prevent bank fees. By keeping it low, I spend less and save more.

Day 17 – Shop your closet

Several years ago, I quit my job to go back to school. Money was tight since I didn’t have an income at the time, so I challenged myself to shop my closet for a year.

This meant that I didn’t buy any new clothes. Instead, I took inventory of everything in my wardrobe, which allowed me to get creative with different outfit combinations and rediscover forgotten pieces.

The first step is to sort through your wardrobe and pull out all your favorite things. These are the items that you tend to reach for the most.

Then make a pile of items that you rarely or have never worn. Try on these items to help you decide if you want to keep, donate, or sell them.

The next step is to gather inspiration from social media, magazines, and Pinterest. For example, if you have a pair of jeans that you love, but rarely wear because you’re not sure how to style them, search for outfit ideas online.

This can help you put together new outfit combinations and get better mileage from your wardrobe.

Day 18 – Work out at home

Finances and money are some of the top things people stress about. According to Tony Robbins, emotion creates motion.

This means if you want to change your state of mind, you need to move your body.

Moving your body is a fun way to release stress and improve your mindset.

Working out at home can be just as effective as gym workouts. It offers more flexibility since you can work out when it’s convenient for you and you don’t have to pay for a gym membership.

I’ve been doing at-home workouts for the past four years and love it. I use the BODi and Peloton app to stream workouts, which is cheaper than paying for a traditional gym membership.

You can also find tons of free at-home workouts on YouTube. This can help teach you the proper form when doing each exercise to stay safe and achieve optimal results.

Depending on your fitness level and available space, you can start by doing body-weight exercises.

If you have the space and you’re ready to invest in gym equipment, Facebook Marketplace can be a great place to find items.

For example, I’ve bought a boxing bag and stand, dumbbells, and a workout bench from Facebook Marketplace. This was cheaper than paying full price at a retail store.

Fitness loop bands can also be a great way to add resistance to your at-home workouts. They’re affordable and easy to store.

Day 19 – Follow the 24-hour rule before buying something

One of the easiest ways to prevent impulse spending and prevent buyer’s remorse is to follow the 24-hour rule.

This means you’ll wait at least 24 hours before buying something non-essential. The rule can help you focus on your financial goals because it interrupts the buying process.

Had a bad day at work? You grab take-out for dinner on the way home because it feels good to eat comfort food without having to cook at home.

A cute dress caught your eye while shopping online? You buy it because it feels good to treat yourself.

When you see something non-essential that you want to buy, instead of reacting in the “heat of the moment” and buying the item, you’re forcing yourself to take a step back and pause.

This allows you to fully consider whether you should make the purchase, and whether it’s a need or a want.

It breaks the cycle of autopilot spending mode and helps you become intentional about the purchase situation.

Read Next: How to stop impulse buying for good

Day 20 – Take inventory of your personal care products

Getting organized and taking inventory of your belongings can be a great way to save money. Below are some of the key benefits:

Declutter – It can help you declutter and get rid of expired products or items that you don’t use anymore.

This can also help you figure out which items you need and which items to put on your “no-buy list”.

For example, nail polish is on my “no-buy list” because I have so many that I won’t be able to use them all before they go bad.

Free up money – By taking inventory of your belongings, this can prevent you from buying new items. Instead, you’ll use up what you already have, which frees up money to spend on other things, like saving or paying off debt.

Become more intentional about your spending – When you see what you already have, this can help you figure out what you actually love and what works best for you.

For example, I got interested in skincare and grew my small collection to over 50+ items in just a few months.

I admit that this was wasteful spending, but I was able to figure out which skincare products worked best for my skin type and which ones to avoid. I was also able to learn how to improve my skincare routine by using the products that already had.

Day 21 – Adjust your thermostat

An easy way to save money is to adjust your thermostat. You can save around 10% annually by turning your thermostat back 7-10 degrees from its normal setting.

In the winter, try keeping your thermostat at 68 degrees while people are home and turning it down to 63 degrees while everyone is sleeping or away from home.

Below are some ways to stay warm without turning up the heat:

- Wear multiple layers of clothing.

- Drink warm drinks (hot water, tea, coffee, etc.)

- Insulate your windows to keep drafts out and the heat inside.

- Seal off unused rooms to keep your main living space warm.

- Use area rugs to keep your living space warm.

- Turn your ceiling fan clockwise to help push hot air down.

- On sunny days, open your curtains to let the heat in.

In the summer, try keeping your thermostat at 78 degrees while people are home and 85 degrees when no one is home.

Below are some ways to stay cool without turning on the air conditioner:

- Stay hydrated by drinking plenty of water.

- Use fans or ceiling fans to keep cool.

- Open windows at night to let the cool air in and create a cross breeze.

- Wear cotton or linen clothing that’ll keep you cool.

- Use insulated curtains or blinds to block out the sun.

- Use a cooling blanket and light sheets for sleeping.

- Eat lighter meals.

Day 22 – Try the pantry challenge

The pantry challenge is where you challenge yourself to eat what you already have in the house instead of ordering take-out or going to the grocery store.

This can help you reduce food waste by using up items before they expire and save money since you don’t need to buy any more food for a length of time.

The first step in starting the pantry challenge is to take inventory of your kitchen. Open your fridge, freezer, and cabinets to see everything that you have.

I find it helpful to make a list and to put an asterisk next to items that are expiring soon (within the month).

The second step is to determine what your schedule will look like over the next few days.

For example, do you have time to finally cook up those dried beans that have been sitting your pantry?

Can you thaw the frozen chicken that’s been hiding at the bottom of your freezer?

Will you get a chance to make homemade vegetable stock with the scraps in your freezer?

It’s important to plan based on your upcoming schedule so you give yourself enough time to prepare your meals without fuss.

The third step is to make a meal plan. Decide what you want to make for breakfast, lunch, dinner, and snacks.

This is important because you don’t want to use up an item at lunch time if you’ll need it to make dinner. Below are some of my favorite pantry meal ideas:

- Soups, stews, and chilis

- Curry

- Enchiladas

- Taquitos

- Quesadillas or burritos

- Tacos (if you have fresh ingredients available)

- Salads (lettuce salads, bean salads, lentil salads, pasta salads)

- Casseroles

- Rice dishes (stir-fry, beans & rice, fried rice, nourish bowls)

- Pasta

- Breakfast for dinner (pancakes, muffins, eggs benedict, waffles, breakfast potatoes, shakshuka)

- Fully loaded baked potatoes

- Grilled cheese or fried egg sandwich

Day 23 – Ask yourself these questions before buying something

Next time you want to make a discretionary purchase or buy something non-essential, asking yourself the following questions can help you be more mindful and intentional with your money.

Why am I here? Are you shopping because you’re bored, feeling sad, hungry, drunk, or you’ve had a bad day?

Am I buying this because it caters to my fantasy self? The version of yourself that wants to be more attractive, assertive, stylish, worthy, smarter, and so on?

Am I buying this because it might sell out? It’s the last one in stock, it’s a limited time offer, or stock is running low?

Am I buying this because it’s on sale? It seems like such a good deal that it would be silly to not buy it.

Am I buying this to feel like I have a sense of control over my life? Buying stuff can provide a false sense of control. It’s better to understand the root cause that’s triggering the lack of control feeling.

Am I buying this to distract myself from something in my life? Turning to retail therapy can make us feel worse over time.

Am I buying this because I want to impress others? Keeping up with the Joneses (needing external validation) will only provide a temporary source of security and won’t make us happy in the long run.

Do I already have something similar? Do I need to replace it right now? If you already have something similar that’s in good condition, then you probably don’t need to buy the new item.

Will I use this item at least 30 times? Consider the lifespan of the item and how you plan to use it. If you only need it for one occasion, then renting or borrowing it might be a better option.

What else can I do with this money? Does it really need to be spent on this item, or would you rather use that money towards paying off debt or saving up for something fun.

Can I afford this? Have I included this in my monthly budget?

Do I have space for this in my home? Where will the item go? Will it add clutter to your home?

Can I rent or borrow this from someone instead of buying it? If you don’t plan to use the item frequently, this can be a great option to save money and prevent clutter.

How many hours of work does this purchase equate to? If you make $20 per hour and the item costs $40, that means the item will cost two hours of your time. Keep in mind there are usually payroll deductions for taxes and insurance.

Will I need to maintain the item? What is the true cost of the item? Maintenance costs can add up over time.

Can this purchase wait? Do you need it right now, or can you get it another time? If it’s on sale, there will always be another sale in the future.

What will happen if you don’t buy this item? Life will go on and you’ll be fine.

Will this purchase lead to more purchases? For example, you buy a new dress and now you need new shoes to match.

Day 24 – Listen to a finance podcast

No matter what your personal finance situation looks like, there are tons of podcast available to help you reach your goals.

This may include learning how to make your first budget, how to manage your debt, saving for retirement, buying a house, or investing for beginners.

Depending on your daily schedule, below are some ideas for when to listen to podcasts:

- During your commute

- Working out

- Walking

- Cooking

- Cleaning

- Household chores

- Shopping

- Waiting

- In the shower

- While working

- Before falling asleep

Day 25 – Read a book about money

While podcasts can be a great way to learn about personal finance, you can dive deeper into the topic by reading a book.

This can help you find better ways to organize your money, plan for retirement, teach your kids about money, tips for managing debt, improving your budget, understanding the psychology of money, and investing.

Below are some of my favorite personal finance books:

- I Will Teach You to Be Rich by Ramit Sethi

- Rich Dad Poor Dad by Robert T. Kiyosaki

- The Total Money Makeover by Dave Ramsey

- Think and Grow Rich by Napoleon Hill

- The Psychology of Money by Morgan Housel

- Beating The Street by Peter Lynch

- Your Money or Your Life by Vicki Robin and Joe Dominguez

- Girls That Invest by Simran Kaur

- The Simple Path to Wealth by JL Collins

- The Millionaire Next Door by Thomas Stanley

Since this is a money saving challenge, I recommend borrowing one of these books from your local library for free.

You can also check to see if there is a used copy available. This can also be a great way to save money.

If you have a busy schedule like me, below are some ways to make time for reading:

- Read before going to bed.

- Always carry a book with you so you can read during your spare time.

- Download an e-reader on your phone or tablet.

- Keep an e-reader in your handbag.

- Listen to an audio book while commuting, working, or doing household tasks.

- Read on your lunch break.

Day 26 – No discretionary purchases above $25 today

A discretionary purchase is something that’s non-essential and not required for basic living.

This includes dining out, personal shopping, entertainment, hobbies, non-essential memberships and subscriptions, travel, gifts, charity donations, and other related spending categories.

Today’s challenge is to not make any discretionary purchases above $25. This means if you want to buy something non-essential today, it must be $25 or less.

Of course you can set your own rules. For example, if $25 seems too high, you can lower it to $10 or $20.

If $25 seems to low, you can raise the amount based on your budget and goals.

You can also choose to do a no-spend day and use that $25 to put towards your savings.

The whole point of this challenge is to force you to be more mindful about your discretionary spending and where you’re putting your money.

Day 27 – Unfollow at least 5 accounts on social media that influence you to buy things you don’t need

Whether you like to admit it or not, social media can have a huge impact on our spending habits.

Depending on who you follow, their content can encourage impulsive or unnecessary purchases.

See someone relaxing on a tropical beach or sitting in a café in Paris? This can make you want to book a trip too.

See someone using a fancy smart watch to crush their fitness goals? This can make you want to buy one too.

See someone wearing a cute dress for weekend brunch? This can make you want to buy a new dress too.

See someone organize their fridge with the perfect clear bins to help reduce food waste? This can make you want to buy them too.

See someone going to a fun concert? This can make you want to buy concert tickets too.

When we see a lot of people on social media wearing designer clothes, staying at 5 star hotels, eating at fancy restaurants, and using top-of-the-line skin care, it can make us feel like luxury is affordable.

Due to this, it can lead people to overspend in order to keep up with their friends and others they see having fun on social media.

While I believe that we should normalize wealth – meaning that we should feel comfortable talking about money and building wealth – it’s also important to live within your means.

If someone can’t afford to pay cash for an item, I’ve seen stores and influencers encourage others to use a “buy now, pay later” service such as Klarna or Afterpay.

Unfortunately, these services can charge late fees for missed payments or interest rates as high as 30%.

Instead of letting friends and influencers tempt you to buy things you don’t need, I recommend unfollowing at least five accounts that encourage impulsive purchases.

I try to get into the habit of unfollowing accounts at the end of each month that no longer serve me. This can be a good way to set boundaries and give you peace of mind so you won’t get triggered by these accounts.

Day 28 – Start a money-mistake jar

A money-mistake jar is kind of like a “swear jar”, where you’ll add coins or money each time you make a financial slip-up.

For example, if you went over your monthly grocery budget, then you’ll add a certain amount of money to your “money-mistake jar”.

Or if you spent money during a no-spend weekend, you’ll add money to the jar.

This can help encourage better spending habits or motivate you to save money. Of course, you want to try your best to avoid any financial slip-ups.

But it’s okay to make mistakes, especially when you’re learning how to get better with money.

The first step in using a money-mistake jar is to set a goal. Do you want to use this jar to help you save more money and avoid further slip-ups?

The second step is to set the rules. Identify the common money mistakes that you make and want to improve. You can use the jar for all financial slip-ups or choose to focus on just one common mistake.

For example, I used to eat out a lot and was constantly going over my monthly restaurant budget. To help me save money, I would add money to the jar each time I would grab take-out instead of cooking at home.

The third step is to choose your penalty. This is the fee that you must add to your jar each time you make a slip-up. Penalties can be either $1, $5, $10, $20, $50, or $100, depending on the slip-up.

The key to changing your spending behavior is to stick to the penalty.

There will be times when you don’t want to add money to the jar or give less than the penalty amount you had originally set. But sticking to the rules will give you the best results.

The fourth step is to make a plan for the money. What do you plan on using the money for in the jar? Setting a clear goal can help motivate you to save and stick to your budget.

Day 29 – Transfer money to an investment account

While being frugal can help you save money, saving alone won’t make you rich.

If you want to build wealth, it’s important to both save AND invest. For beginners, I recommend looking into low-cost index funds when starting an investment portfolio.

In the meantime, putting your savings into a high-yield savings account can be a great idea. This will allow your money to accumulate interest instead of keeping it in a checking account or regular savings account.

Day 30 – Review your budget and make adjustments

A budget is a tool that can help you reach your financial goals. This means that it shouldn’t be set in stone. As your needs, wants, and goals change, your budget may need to change too.

It’s a good idea to get into the habit of regularly reviewing your budget and creating a new one for each month.

Changes in your life or financial situation is also a good time to update your budget.

For example, when I had a baby, my budget needed to reflect this change. Both my fixed and variables expenses needed to be adjusted to make room for essential baby items.

Some things you may want to consider when reviewing your budget include:

- Your expenses (Have they gone up or down?)

- Your income (Have you started a new side hustle? Did you get a pay raise at work? Have you taken a recent pay cut?)

- Life changes (Did you leave a job or get a new job? Did you have a baby? Did you move to a new home? Did you get married or divorced? Are you taking a course or have gone back to school?)

- Your financial goals (Is your budget still helping you reach your goals?)

- Your spending habits (Are you able to stick to your budget? Are there areas of your budget where you tend to overspend or underspend?)

With these things in mind, this can help you make the appropriate adjustments to your budget.

Related Posts: